At the end of this year, I gave myself a target of pocketing $1100 of dividend. After the last wave of results for all my companies, I have collated the dividends received and in 2017, I have received a total of $1083.87. A little shy of the $1100 target!

Achieving this target was not easy in 2017 as one of my core holdings, Singapore Post, decided to peg dividend payout to earnings rather than a fixed rate. SingPost paid out $0.065 of dividend in 2016 compared to $0.020 in 2017. I patched this hole mainly by deploying more capital this year and scoring a buy in Silverlake Axis. Silverlake Axis has its best dividend yield for years due to its divestment of GIT, with a $0.048 payout or 8.18% according to StocksCafe. Myself, I reaped a 7.19% dividend yield as I missed the first payout this year.

Other notable stock was Karin Tech where it distributed 10.28% of dividend. I have absolutely no idea how they maintain this level of dividend till today, but it is still serving me well despite many years of skepticism.

All said and done, I am satisfied getting more dividends this year and all this was to ensure that I can increase my dividend gradually and eventually able to reap enough passive income to be financially independent. You should starting working on yours too!

Saturday, 18 November 2017

Wednesday, 18 October 2017

Things I Learnt At My New Place of Employment

Since August, I had actually switched career from Transportation/Logistics industry to the Finance industry. Though it is more of a middle-to-back office function, there were many things I learnt in office which I am starting to apply in my own portfolio tracking (not stock picks!)

1) Benchmarking

In my company where institutional funds are being managed, there must be a way to tell the client we are performing better, and that is where benchmark comes into play. When buying into a fund/equity, the benchmark has already been decided. In my case where I buy mainly local equities, STI Index will naturally be what I will compare against - you will hope that you will perform better, if not you are better off buying STI ETF. However, if you buy into US equities or HK equities, additional benchmarks have to be brought in to compare against.

With this benchmarking process, it has definitely brought another extra level of stress to the investing journey. Back in the earlier days, a gain is a gain and I will be happy. Now, even if it is a gain, "did I perform better than STI Index?", "am I losing STI Index at the portfolio level?".

Despite this, I can commit to a higher level of investing picks knowing that there is something I have to beat. That, and also the universe of benchmarks I can refer at work!

2) Asset Allocation

Based on the client's needs, the team will decide what is an appropriate asset allocation of the portfolio. Pension funds? Choose predominantly income funds with little capital risk and stable income so that monthly pension can be distributed. Investment vehicle of company? Avoid income stocks, increase growth drivers, Emerging Markets etc.

So how can I use this on a personal basis or how can I adapt this into my monthly portfolio tracking?

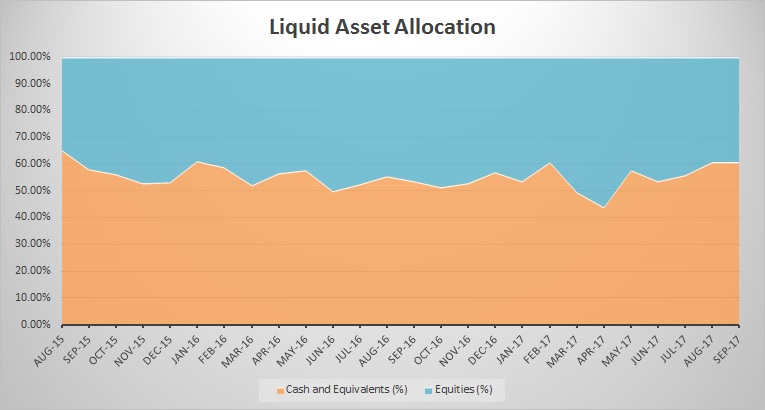

Using my monthly records tracing back to 2 years ago, I further calculated what was actually my asset allocation. Being a retail investor there was not much asset classification I could choose from. It will probably be Equities, Cash and Bonds. I could further break my equities into strategy groups as per my example above much it would not make much sense due to my limited capital.

When the chart above was generated, I was actually pleasantly surprised at how consistent the allocation was! My total asset was not stagnant as I had transition from a student to a working adult in this two years of data. I was not tracking the allocation at all. But subconsciously, I was able to move my asset around to achieve that consistent level of allocation.

When my first salary started, I actively sought stocks to invest in. When I overbought stocks, I try to sell away one other counter to balance my exposure. Somehow along the way, I maintained this average Equities allocation of 44%.

While I looked like I did not need this asset allocation, what I learnt at my workplace is to have the discipline to set the allocation and follow it, subject to any review. While I am more comfortable at the current allocation between Equities and Cash, I know I should either 1) Increase allocation to Equities or 2) Move some cash and diversity into Bonds. This is because as a young adult, I should be taking on high risk given my long investment horizon. Either of these two methods will make my cash work harder and I will be taking some action soon.

3) Tracking Portfolio Properly

The last thing I learnt from office was probably how to properly track my portfolio. This is primarily because I learnt the different classification types that the investment team uses, and slowly adopt it to mine!

Some difficulties I faced before was to include or exclude:

- CPF

- A sum of money that someone owes me, and

- Cash value of my insurance policy

In my old tracking, I included the last two assets accounts but not CPF, as part of my Total Assets. In addition, I lump all the monies into a single number as displayed below.

Now that I have some sort of structure to my asset classification, I wanted to retain the use of the Cash and Equities composites in my Total Assets record. After a few days of side thoughts while working, I decided to classify the 3 pointers above as Illiquid Assets, in addition to the Cash and Equities asset class. The below chart was the last change I did to my net worth tracking.

With this I am able to visualize how each of these asset types makes up my Total Assets while being able to monitor the total asset growth. For myself, it is very interesting to see how my CPF begins to balloon in size after I entered the workforce.

Another unsettling observation I can draw from this is that CPF is a growing component of my Total Assets. In theory, CPF should contribute 17% + 20% of my basic salary. My take home salary should be 83% of basic salary. A quick conclusion will be that I am spending a lot such that CPF grows relative to my liquid assets! (On hindsight, it might be the $5,000 NSmen incentive).

In this post, I shared what are some of the lessons I brought home from work. As my tenure grows, I foresee I will try out more features which I taught will be useful. It is exciting and fulfilling to have enjoy what I do at work and I hope this feeling will be here to stay. As Dow continues to march towards 23,000, let's put on our critical hat and start to fear when everyone is greedy.

Sunday, 20 August 2017

Review of my Sitra Holdings Purchase (5LE.SI)

I rarely buy any stocks based on people's recommendation, at least not without going through their rationale first. However recently, I bought Sitra Holdings based on the call made by The Little Snowball. Their case made for Sitra was fair and substantiated by (or very similar to) previous analyses found here and here. I entered at $0.017.

Disappointingly, Sitra's 1H2017 results did not deliver as expected, with losses increasing from $245,000 to $643,000.

Voluntary Salary Deduction

While most analyses had been lauding the company's steady trajectory to an eventual profitability, they have missed out a component enabling that - voluntary management's salaries reduction. Senior management previously took a pay cut to ease the finances of the company. These voluntary salary deductions were reinstated in the latest set of results and indeed, selling and marketing expenses together with administrative expenses increased.

Senior management reinstating their salary arrangements may be a good sign that company is turning around and they are more comfortable receiving their original salary. However, this factor may have been "beautifying" previous results and maybe the path to profitability may not be as straightforward after all.

Forex Losses

While results were not fantastic in this half year, peeling back the forex losses will reveal a nicer set of numbers. Ignoring forex losses of $0.43M parked under other losses - net, the losses narrow to $213,000 which is definitely an improvement from the previous 1H result.

Conclusion

Taken together, it is fair to conclude indeed, the finances of the company are improving if the above two points were factored out. However, senior management fees should be the rule rather than exception and hence the company do have to work a bit harder to eke out profits.

Looking at the cash flow statement, Sitra only has $2,000 cash at the end of the period, paralyzed by high trade receivables and bank overdrafts. This is another area that the company has to brush up on to survive the next economic downturn. Hopefully, rights issue will not be called as I do not hope for a long-drawn investment in Sitra. If need be, I am willing to dispose this stock at a loss as my capital outlay is purposely kept small due to the speculative play.

Saturday, 22 July 2017

Half-Year Portfolio Review

Half-Year Portfolio Review

2017 was the first full year that I am working full-time and this has taken time away from my investment hobby and more or less contributed to a poor performance against the STI. As I had written in haste previously, I bought and sold stocks in frenzy in order to ride the wave of the bull market. Thereafter, I calmed down slightly to properly review my portfolio and make a mental note of which is a investment stock and which is a trading stock. For myself, I separate my stocks according to these two types and my strategies differs respectively.Investment Stock -

- Stocks are researched to some degree before buying

- Investment horizon is generally longer

- Willing to take some loss in order realise the supposed value (current limit is 30%)

- Embarrassingly, I do not have a proper exit plan yet (this is the reason for why SingPost is utterly dragging my portfolio down or else I usually wait for an event that trigger me to sell ie. takeover, market starts turning down)

- Recent example: Tianjin ZX, ST Engineering, Falcon Energy and HPH Trust

Trading Stock -

- Stocks are bought on sentiments though I do make sure there are some safety nets like an existent dividend yield and reasons for the stocks to chiong

- Usually sold when there is a quick gain

- Stop-loss limit to a tune of -5% or when I know there is no longer any impetus for stocks to chiong

- Recent example: HC Surgical, M1, HRnetGroup (I bought and sold M1 and HRnetGroup within such a short window that I did not update here)

When I group the stocks according to my objectives, I am more prepared when the prices actually hit the sell price, be it a profit or a loss. Therefore, I advocate to investors out there to know the difference between investing and trading. While I had advocated for a investment slant, I do trade from time to time to feed the itch.

Dividends

In my 2016 Investing Report Card, I had made $1100 as the dividend target to hit this year. As of me writing this post on 16 July, I have accumulated $635.39 in dividend or 57.76% of the target. While it is lagging behind the time equivalent of the year, it will catch up eventually as some stocks do not declare every quarter. However, given the poor performance of SingPost, I will eventually miss my dividend target this year unless I heavily increase my capital. I am not inclined to do so as the market is very high right now.

Performance

For the first 6 months this year, I have accumulated a XIRR of 2.867%. This return is abysmal compared to the general market. This is really attributed to the fall of SingPost, which is frankly quite unrelenting. SingPost has been the gem in my portfolio and I have refused to sell it despite the many pitfalls and signs it had been displaying. The advice of not falling in love with any particular stock is really true in this case and I have been considering to write a post on how to sell a stock in order to keep myself disciplined.

However, as I am only writing this half-year review post now in July, there had been a offer for GLP to be taken private amongst other movements and I hope it will contribute to an improved full year returns.

So that's all for my half-year review. STI has been huat huat for a while now and I feel that there are increasingly lesser value stocks around. The theme should switch to hunting turnaround stories as the bullish market will handsomely reward these turnaround. At the same time, we should be nimble in our buying or selling so as to not be caught off guard if the market turns. All the best in your investing journey!

However, as I am only writing this half-year review post now in July, there had been a offer for GLP to be taken private amongst other movements and I hope it will contribute to an improved full year returns.

So that's all for my half-year review. STI has been huat huat for a while now and I feel that there are increasingly lesser value stocks around. The theme should switch to hunting turnaround stories as the bullish market will handsomely reward these turnaround. At the same time, we should be nimble in our buying or selling so as to not be caught off guard if the market turns. All the best in your investing journey!

Saturday, 24 June 2017

Tianjin Zhongxin Pharmaceutical (T14.SI)

Tianjin Zhongxin Pharmaceutical (T14.SI) is engaged in the development, manufacture and distribution of mainly Chinese traditional medicine. In addition to Chinese medicine, its products also include distribution of Western medicine operated jointly with pharmaceutical giants like GSK and Baxter.

Pharmaceuticals in SGX are far and few between and Tianjin ZX certainly piqued my interest. It first appeared in my radar while searching for stocks that have not ran up in this bull market, dividend-yielding, EPS growth in the past 5 years, reasonable market capitalization and in profit. Among all the stocks that appeared, Tianjin ZX had a good economic moat expected. of a pharmaceutical firm.

Digging up the past year's performance, Tianjin ZX was quite impressive as well.

Pharmaceuticals in SGX are far and few between and Tianjin ZX certainly piqued my interest. It first appeared in my radar while searching for stocks that have not ran up in this bull market, dividend-yielding, EPS growth in the past 5 years, reasonable market capitalization and in profit. Among all the stocks that appeared, Tianjin ZX had a good economic moat expected. of a pharmaceutical firm.

Digging up the past year's performance, Tianjin ZX was quite impressive as well.

In 2010, the Company reported 0.4 RMB in earnings. This rose to a high of 0.6 RMB in 2015 before dipping to 0.55 RMB in 2016. As shown in the graph above, NAV displayed an even better result. The Company grown from 2.43 RMB in 2010 to 5.38 RMB in 2016. This represent a CAGR growth of 14.16%.

S-chip is still viewed suspiciously by many in Singapore. Most recently, Eratat declared that it has no assets to be distributed to shareholders and delisted without any resolution to them. The cash declared to be held in banks were non-existent. However, Tianjin ZX pays a steady dividend year and this should imply that the cash were certainly present. For year of 2016, Tianjin ZX paid a dividend of 0.25 RMB. This is subjected to a 10% tax rate in Singapore and should amount to a final dividend of 0.225 RMB. At my buy price of 0.965 USD, this will translate to approximate yield of 3.4%.

At current valuation, Tianjin ZX has a P/E of 11. For a pharmaceutical company, this P/E is somewhat low and have upside potential. For the latest quarter, the Company holds 536,481,000 RMB of cash, approximately 10% of share price. However, the crux of my purchase lies in this fact. Tianjin ZX is also listed in Shanghai at 17.65 RMB or S$3.58. At 0.US$965 or S$1.35, Tianjin ZX is listed in SGX at a 62% discount and 31.52 P/E!!!! I do not understand what caused the extent of this different valuation. However, I do hope that management will buyout my shares in and relist them at Shanghai for better returns.

All this said, Tianjin ZX has been facing lower revenue but have been compensating by increasing operating efficiency and cost-cuts, leading to higher gross profit margins. In the latest quarter results, Tianjin ZX revealed that it is under challenging economic conditions and competitive environment. It is aiming to overcome these with the following actions:

- Placing greater emphasis on innovation and creation and establishing the importance of scientific development;

- Strengthening its marketing plans to increase the amount of industrial sales so as to create more profits for the Company;

- Focusing on research and development activities to enhance the Group’s core competitiveness in technology;

- Strengthening the internal controls and management of the Group

Writing this post, I hope that Tianjin ZX will be deserving of my long-term investment and reap future returns.

Sunday, 2 April 2017

Frenzy State

Caught up in a company project, I have not been devoting time to investing as much as I would like it to be. However, these past months, it had been disheartening to see the stock market rocketing while my portfolio languish due to legacy stocks and staying on the sidelines.

I've also been kicked a hard lesson with regards to doing my homework before investing in anything. I admit that I have been caught up in the frenzy of stock market, buying stocks without so much as doing some calculations. This few months, I had actually did some shuffle in my portfolio without much research.

Here are some of my transactions I did without announcing it here due to a lack of time. From hindsight, most are of poor choice and I really attribute it to the lack of steadfastness in this volatile stock market.

1) Sold ST Eng @ $3.62 (Wanted to take some profits off the table)

2) Sold Falcon Energy @ $0.128 (I capitulated on this stocks due to the poor outlook, it is not impossible to see this below 10c given the poor performance. However, it did rebound strongly last week to my dismay)

3) Bought Far East Orchard @ $1.685 (Bought on the day some cooling measures were announced. I have eyed this stock for a while due to it trading at a strong discount to book. Good dividend every year. Took into account some measure of takeover play as well)

4) Bought Serial System @ $0.186 (Sam Goi has been buying into it. It has a stable dividend history with good volume. Rare that a stock being "played" has a good dividend payout. Bought it with the hope of riding on Sam Goi's wave)

5) Bought Silverlake Axis @ $0.57 (Technology stock, steady dividend though business has deteriorated. Given that the economy seems to be recovering, a strong comeback in banks may give this stock some business. Waiting for the special dividend as well. Good potential overall with most risk due to its legacy short-seller's report)

As you can see, my investing has been haphazard and I am not proud of it. It is definitely not me. But the lack of time to invest, coupled with colleagues that check stock and telling me about their returns, coupled with the fear of losing out in the market spurred me to do this transactions. Hopefully they do not fail me. Last thing I want is to be caught in the peak of market as many had done before me. As of now, the stocks I had bought are not at astronomical valuation but it is not with the same level of undervalued-ness I had bought before.

Sunday, 29 January 2017

Saturday, 7 January 2017

HC Surgical Specialists Limited (1B1.SI)

HC Surgical Specialists is a a medical services group primarily focusing on endoscopic procedures through a network of 12 clinics in Singapore. These clinics are distributed across heartlands and also in major private hospitals. In addition, the company has entered into a MOU with an independent party to provide training and consultancy at Transport Hospital in Vietnam. Their specialist surgeons will be registered to practice at the hospital and help set up a day surgery and endoscopy centre, thereby securing the exclusive rights to perform surgical and endoscopic procedures for a period of time.

Rational for Purchase

Bought this stock hastily on 6 Jan 2017 to take advantage of the $0.018 declared dividend. At my purchase price of $0.625, it is a 2.88% dividend yield - good for a growth and healthcare stock. I had only analyzed this stock retrospectively (flouting the rules, need to reflect on myself). Besides the attractive dividend for a healthcare stock, this stock caught my attention due to its similarity to another successful IPO by Singapore O&G, attaining multi-bagger returns.

- Both are companies related to healthcare, though Singapore O&G focuses another field

- Both had IPO price in the $0.20-$0.30 range

- Both trading at P/E in excess of 30

- Both declares dividend

- Singapore O&G traded in the $0.60 range when it first debut

With these similarities, I am hoping HC Surgical Specialist will replicate the price trajectory as well.

On a more fundamental basis, HC Surgical is good due to the following reasons.

- Singapore is an ageing society, with more need for healthcare

- Specialist medical services

- Entry into Vietnam with clear business outlook

This is a superficial comparison that I should be ashamed of, but since my Buy Order was unexpectedly triggered, why not I publish this here as a record.

Financial Performance

I had briefly looked through the half year financial statement before the purchase. With a quick peek, I gulped at the bottom line, with a 98.5% drop. I knew there was an IPO expense but did not have the time to add it back to compare. Now that it is the weekend, let's sit down and go through the numbers.

IPO expense was $1.258M. Adding it back to profit before income tax, it comes up to $1.357M - still 15% lower than the previous year. I factored in an increase tax expense to reach end profit of $1.357M. With outstanding shares post-IPO of 146,311,530. The EPS comes up to $0.0075 for the half year ended 30 Nov 2016.

Assuming consistent earning at the second half, the P/E at $0.625 is a whopping 42 - really going against my usual theme of value investing.

The declared dividend policy is to pay out 70% of its profit. With my estimated EPS of $0.015, the dividend payout is nearly 120% of profit. So this $0.018 dividend essentially has some parts coming out of the IPO proceed and I should not expect this rich a dividend in the future.

Maybe I have been pessimistic since finance costs will likely go down in subsequent quarters. New subsidiaries will boost earnings (with a chance expenses outpace it) and entry into Vietnam presents growth. But overall, I had find my purchase rather risky and not entirely based on fundamentals. Rather, it is speculative based on my comparison to Singapore O&G. In addition, HC Surgical had declared that "operating environment of the medical industry to remain challenging in the next 12 months..."

However, a buy is a buy and I will like to see this stock still emulating the trend of Singapore O&G for a better Goat Year!

Sunday, 1 January 2017

2016 Investing Report Card

Year 2016 Closes, Results and Returns

2016 closes and with SGXcafe calculating returns on a daily basis, I knew what was coming before the year ended. Disappointingly, my portfolio underperformed STI ETF returns this year - the first time since 5 years of investment. With the negative losses last year, it was quite disappointing to have not grown my investment this year as well.2016 Portfolio XIRR: -2.215%

STI ETF XIRR: 2.864%

Fun Facts

For now, let's lighten up the mood for some infographic about my portfolio movement this year:

Dividends Goals

With regards to $1000 the dividend goal I had set for 2016, you can see that I have narrowly missed it with $954.25. This partly due to Singpost's tightening dividend policy as well as Falcon Energy not yielding any dividend this year.For 2017, I hope to increase my dividend received to the tune of $1100. Building up a portfolio that can gives me a steady income stream is one of my retirement goals for the long long term, and I hope that I am able to slowly accomplish this goal.

To increase the dividend, one way is to focus on purchasing stocks that are dividend-yielding and have the cash flow to support it. Monthly investment in STI ETF with my siblings will also contribute in a minor way, probably to cover the shortfalls from the dividend cut by Singpost.

Going Forward

Despite these two years of negative returns, I aim to keep the course. But it has certainly made me re-assess the way I look at gains. A problem is me not realizing profits only to watch it slip away and never coming back. One part of me always wants to be noble and be a "long-term investor". The other part is Graham's and Buffet's mantra of only buying companies where you will never give it up. Falcon Energy has been a bummer and I hope it proves itself in 2017.

For further pickings, I have a few stocks in my mind for research and considerations. Working gives me an steady income to invest but it takes time away from research and homework. But I hope to stay the course and just keep moving ---- towards financial freedom!

Subscribe to:

Comments (Atom)