1) Benchmarking

In my company where institutional funds are being managed, there must be a way to tell the client we are performing better, and that is where benchmark comes into play. When buying into a fund/equity, the benchmark has already been decided. In my case where I buy mainly local equities, STI Index will naturally be what I will compare against - you will hope that you will perform better, if not you are better off buying STI ETF. However, if you buy into US equities or HK equities, additional benchmarks have to be brought in to compare against.

With this benchmarking process, it has definitely brought another extra level of stress to the investing journey. Back in the earlier days, a gain is a gain and I will be happy. Now, even if it is a gain, "did I perform better than STI Index?", "am I losing STI Index at the portfolio level?".

Despite this, I can commit to a higher level of investing picks knowing that there is something I have to beat. That, and also the universe of benchmarks I can refer at work!

2) Asset Allocation

Based on the client's needs, the team will decide what is an appropriate asset allocation of the portfolio. Pension funds? Choose predominantly income funds with little capital risk and stable income so that monthly pension can be distributed. Investment vehicle of company? Avoid income stocks, increase growth drivers, Emerging Markets etc.

So how can I use this on a personal basis or how can I adapt this into my monthly portfolio tracking?

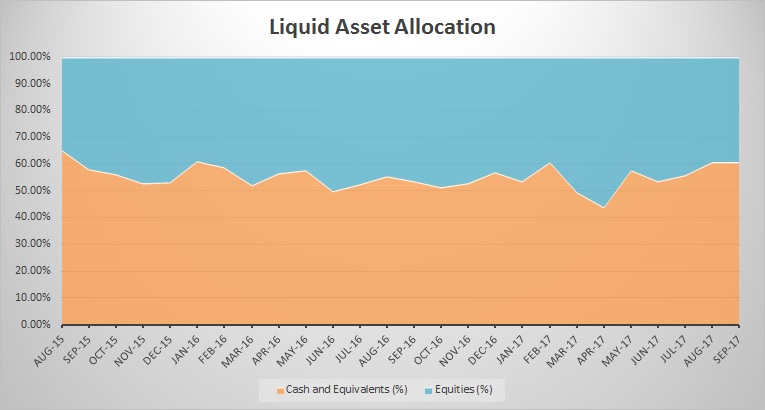

Using my monthly records tracing back to 2 years ago, I further calculated what was actually my asset allocation. Being a retail investor there was not much asset classification I could choose from. It will probably be Equities, Cash and Bonds. I could further break my equities into strategy groups as per my example above much it would not make much sense due to my limited capital.

When the chart above was generated, I was actually pleasantly surprised at how consistent the allocation was! My total asset was not stagnant as I had transition from a student to a working adult in this two years of data. I was not tracking the allocation at all. But subconsciously, I was able to move my asset around to achieve that consistent level of allocation.

When my first salary started, I actively sought stocks to invest in. When I overbought stocks, I try to sell away one other counter to balance my exposure. Somehow along the way, I maintained this average Equities allocation of 44%.

While I looked like I did not need this asset allocation, what I learnt at my workplace is to have the discipline to set the allocation and follow it, subject to any review. While I am more comfortable at the current allocation between Equities and Cash, I know I should either 1) Increase allocation to Equities or 2) Move some cash and diversity into Bonds. This is because as a young adult, I should be taking on high risk given my long investment horizon. Either of these two methods will make my cash work harder and I will be taking some action soon.

3) Tracking Portfolio Properly

The last thing I learnt from office was probably how to properly track my portfolio. This is primarily because I learnt the different classification types that the investment team uses, and slowly adopt it to mine!

Some difficulties I faced before was to include or exclude:

- CPF

- A sum of money that someone owes me, and

- Cash value of my insurance policy

In my old tracking, I included the last two assets accounts but not CPF, as part of my Total Assets. In addition, I lump all the monies into a single number as displayed below.

Now that I have some sort of structure to my asset classification, I wanted to retain the use of the Cash and Equities composites in my Total Assets record. After a few days of side thoughts while working, I decided to classify the 3 pointers above as Illiquid Assets, in addition to the Cash and Equities asset class. The below chart was the last change I did to my net worth tracking.

With this I am able to visualize how each of these asset types makes up my Total Assets while being able to monitor the total asset growth. For myself, it is very interesting to see how my CPF begins to balloon in size after I entered the workforce.

Another unsettling observation I can draw from this is that CPF is a growing component of my Total Assets. In theory, CPF should contribute 17% + 20% of my basic salary. My take home salary should be 83% of basic salary. A quick conclusion will be that I am spending a lot such that CPF grows relative to my liquid assets! (On hindsight, it might be the $5,000 NSmen incentive).

In this post, I shared what are some of the lessons I brought home from work. As my tenure grows, I foresee I will try out more features which I taught will be useful. It is exciting and fulfilling to have enjoy what I do at work and I hope this feeling will be here to stay. As Dow continues to march towards 23,000, let's put on our critical hat and start to fear when everyone is greedy.